🏠 The Secret Safety Net Every Renter Needs

You’ve signed the lease, paid the security deposit, and picked out the perfect spot for your favorite armchair. You’ve done everything right. But there’s one document you might have skimmed, ignored, or actively avoided: the renter’s insurance policy.

For many renters, insurance feels like just another bill—an optional expense that goes straight into the “unnecessary” pile. After all, the building itself is insured by the landlord, right? What could possibly go wrong that necessitates paying extra?

This line of thinking is not just omnipresent; it’s a dangerous and costly misconception.

Renter’s insurance is arguably the single most important and least expensive tool for protecting your financial life. Yet, it’s obscured by myths that prevent people from getting the coverage they desperately need. Your landlord might require you to have it, but they often won’t take the time to explain what it actually covers.

We’re here to bust the most pervasive myths and reveal the truth about this essential safety net. If you think renter’s insurance is expensive, unnecessary, or only covers your TV, prepare to be surprised.

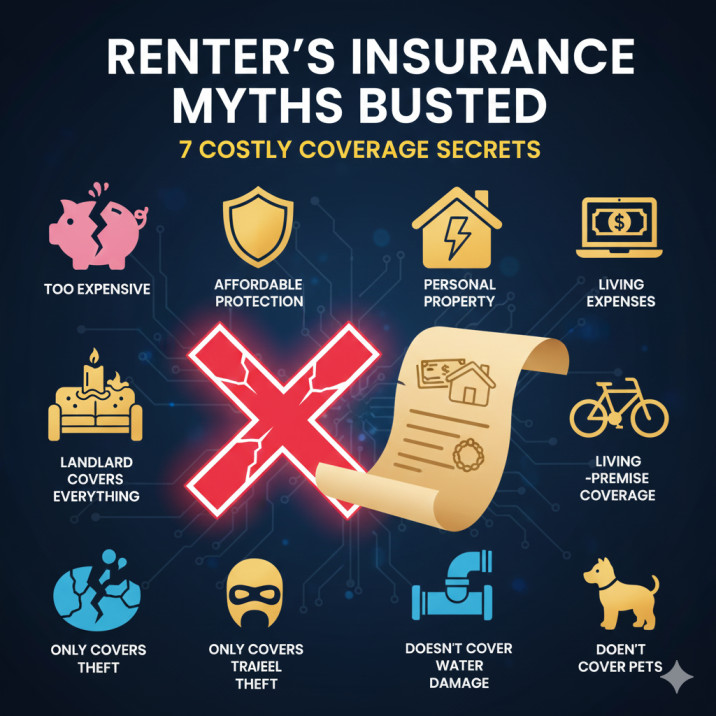

Myth 1: “My Landlord’s Insurance Covers Everything I Own.”

❌ FALSE

This is the most common and financially devastating myth. It’s the reason why, after a fire or burst pipe, renters often find themselves homeless and broke.

- The Landlord’s Policy (Dwelling Coverage): Your landlord’s insurance only covers the physical structure of the building itself. It covers the walls, the roof, the fixed plumbing, the appliances owned by the landlord, and liability for accidents in common areas.

- The Coverage Gap: The landlord’s policy stops at the structure. It does not cover the contents inside your unit. If a fire starts in the kitchen and destroys your furniture, clothes, electronics, and priceless vinyl collection, your landlord’s insurance will rebuild the kitchen, but they won’t replace a single sock you owned.

Renter’s Insurance (Contents Coverage) is the only thing that covers this gap. It covers the cost of replacing your personal property after a covered peril, whether it’s a fire, smoke, theft, or vandalism.

Myth 2: “Renter’s Insurance is Too Expensive.”

❌ FALSE

Compared to auto insurance, home insurance, or even a monthly streaming subscription, renter’s insurance is surprisingly affordable.

- The Real Cost: The national average cost for a standard renter’s insurance policy is typically between $15 and $30 per month—or roughly $180 to $360 per year. That’s less than the price of two specialty coffee drinks a week.

- The Value Proposition: For the price of a takeout meal, you get $25,000 to $50,000 worth of personal property coverage and hundreds of thousands of dollars in liability protection. Considering the average American owns approximately $20,000 to $30,000 worth of contents, this is an unbeatable bargain.

- Cost-Saving Tip: You can often bundle your renter’s policy with your auto insurance for a multi-policy discount, making the effective cost of the renter’s policy even lower.

Myth 3: “I Don’t Own Enough Expensive Stuff to Make it Worth It.”

❌ FALSE

Most people drastically underestimate the aggregate value of their belongings. We tend to focus on the big-ticket items, but the true cost of replacement lies in the sheer volume of everyday necessities.

- The “Stuff” Inventory: Do a quick mental inventory: your wardrobe, pots and pans, bedding, towels, books, sneakers, toiletries, and small kitchen appliances. If you had to buy all of that new today, the cost would skyrocket.

- The Replacement Cost Difference: Most policies offer Replacement Cost Value (RCV) coverage, meaning the insurer pays you the cost of buying a brand new equivalent item, without deducting for depreciation. This is essential, as the Actual Cash Value (ACV) would leave you with significantly less money.

- Pro-Tip: Make a Digital Inventory. Walk through your apartment with your phone and video-record everything, opening drawers and closets. This simple step makes the claims process infinitely faster if disaster strikes.

Myth 4: “My Belongings Are Only Covered When They Are Inside My Apartment.”

❌ FALSE

This is one of the best-kept secrets of renter’s insurance: your coverage is portable, protecting your belongings outside the rental unit, virtually anywhere in the world.

- Off-Premises Coverage: Renter’s policies typically include a percentage (often 10% to 20%) of your total personal property coverage for items you take with you.

- Example 1: If your laptop is stolen from your car while you are visiting a coffee shop, your renter’s insurance can cover it (after your deductible), even though the incident didn’t happen in your apartment.

- Example 2: If your luggage, containing thousands of dollars in clothing and electronics, is lost or stolen during a vacation overseas, your renter’s insurance can cover the loss.

- Important Note: The deductible still applies, and expensive single items like high-end jewelry or professional camera equipment may require a separate endorsement (sometimes called a floater or scheduled personal property) to be fully covered.

Myth 5: “Renter’s Insurance Only Covers Theft and Fire.”

❌ FALSE

While theft and fire are the most common reasons people file claims, the most valuable part of the policy is often the coverage you never thought you needed: Liability and Loss of Use.

Coverage Component 1: Liability Protection (The Lawsuit Shield)

This is the true financial lifeboat of the policy. It protects you financially if you are found legally responsible for injury or property damage to someone else, inside or outside your unit.

- Examples of Liability Claims:

- Guest Injury: Your friend slips on a wet spot on your kitchen floor, breaks their leg, and sues you for medical bills and lost wages.

- Property Damage to Others: You accidentally overflow your bathtub, causing thousands of dollars of water damage to the apartment below yours.

- Pet Incidents: Your dog bites a delivery person on your property.

Liability coverage typically starts at $100,000. This coverage pays for legal defense costs and any settlement or judgment against you, up to your policy limit. Without it, you could be financially devastated by a simple, everyday accident.

Coverage Component 2: Loss of Use (The Hotel Bill Savior)

What happens if a fire or a major water leak makes your apartment uninhabitable for a month? Where do you go?

- What it Covers: The Loss of Use (or Additional Living Expenses, ALE) portion of your policy pays for temporary housing, meals, and other necessary expenses if you must vacate your rental while it’s being repaired after a covered loss.

- The Cost: This coverage can pay for the cost of a hotel or a short-term rental unit. Losing your home is stressful enough; the ALE coverage ensures you don’t also have to worry about finding the money for temporary lodging.

Myth 6: “My Roommate Already Has Renter’s Insurance, So I’m Covered.”

❌ FALSE

This depends heavily on how the policy is written, but in most cases, a standard policy only covers the named individuals.

- Named Insureds: Most renter’s policies will only cover the belongings of the people specifically named on the policy. If your roommate buys a policy in their name alone, their clothes, computer, and furniture are covered—but yours are not.

- Joint Policies: If you and your roommate are listed on the lease, you can often be added to the same renter’s insurance policy. This is usually the easiest and cheapest option. However, if one of you moves out, the policy must be updated immediately.

Rule of Thumb: If your name is not on the insurance document, your stuff is not covered. Always verify your status on the policy.

Myth 7: “The Landlord Just Requires it So They Can Get a Check From Me.”

❌ FALSE (Mostly)

While landlords benefit from the reduced risk, the true reason they require it is to protect themselves from your liability.

- Protecting Their Investment: If you cause a fire that damages the building, their insurance company will pay to fix the property, but they will then turn around and subrogate (sue) you to recover the money.

- The Landlord’s Expectation: By requiring you to have a liability policy (renter’s insurance), the landlord ensures that if you accidentally burn down the kitchen, your insurance company, not your personal bank account, pays for the damage to the building. This is a crucial risk transfer mechanism that safeguards both parties.

The Final Word: Take Control of Your Financial Safety

The Attention Economy may trick you into spending $20 a month on streaming subscriptions, but the Attention Economy won’t replace your furniture after a kitchen fire.

Renter’s insurance is not a luxury; it is a foundational element of financial stability for anyone who doesn’t own the dwelling they live in. It’s affordable, it’s comprehensive, and it protects you from the potentially bankrupting consequences of a disaster you can’t control.

Don’t wait until you’re standing in front of your damaged apartment, realizing that your $20,000 worth of possessions is now a total loss. Call an insurance agent or get an online quote today. For less than a dollar a day, you can finally plug the most dangerous financial hole in your renter life. Your landlord won’t tell you the myths, but they know you need the protection.